The Fire Mark

In 1752 Benjamin Franklin's insurance company priced exposure on verifiable features and bolted a metal plaque to the wall. The mechanism worked. California has broken every link in it.

On April 13, 1752, twelve Philadelphia gentlemen — including a forty-six-year-old printer and recently retired postmaster named Benjamin Franklin — met to organize what they called the Philadelphia Contributionship for the Insurance of Houses from Loss by Fire. The first Board of Directors met for the first time on May 11. The Deed of Settlement bound the subscribers into a mutual: each policyholder was both insured and insurer, capital came from up-front deposits, claims were shared in proportion to coverage.

The Contributionship is still in continuous operation today. It is the oldest property insurance company in the United States. The institution that Franklin and his partners organized in 1752 has paid claims continuously through the American Revolution, the Civil War, the 1906 San Francisco earthquake, two world wars, and every California wildfire of the past century. Two hundred and seventy-four years.

What they got right at the founding is what California has been quietly breaking since the 1970s. The Contributionship invented modern American fire insurance with a verifiable price signal — and the verification was structural to the product, not an afterthought.

This essay is about what the Fire Mark actually did, why the mechanism worked, how it eroded, and what the work of rebuilding it looks like in 2026.

The mark on the wall

The Contributionship's hallmark — bolted to every insured house — was a small metal plaque called the Fire Mark. The Contributionship's particular version was four gilded hands, each clasping the wrist of another, arranged in a square on a black shield. Insurance historians call it the Hand-in-Hand. The four hands represented the four-policyholder mutual structure: each member's policy was secured by the joint capital of the others.

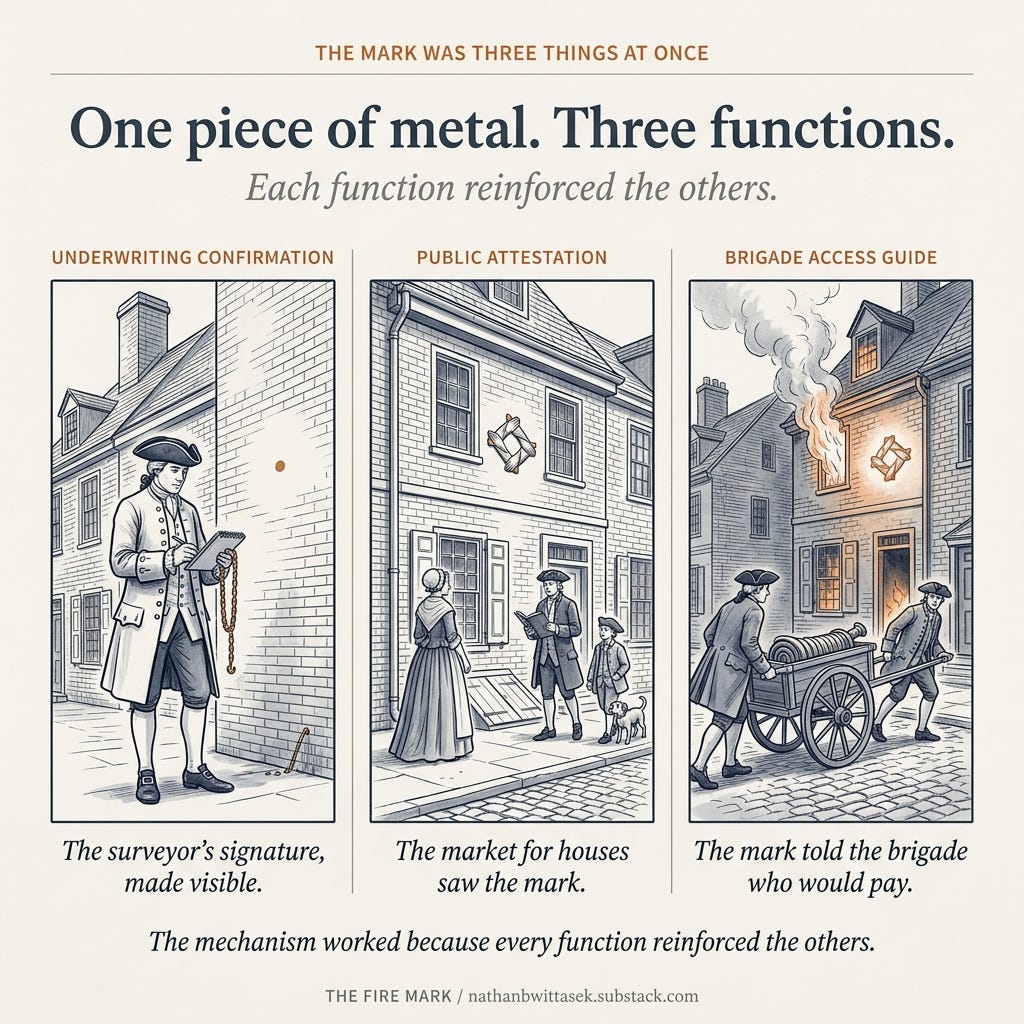

The mark was not decoration. It was not advertising. It was three things at once.

It was an underwriting confirmation. The Contributionship would not insure any house not approved by one of the company's two surveyors — the term they used for what we would today call an underwriter-inspector. The surveyor walked the property, examined the construction, looked at the chimneys, the access to the roof, the proximity to outbuildings, the condition of the masonry. If the property passed, the surveyor signed. The Fire Mark was the surveyor's signature, made visible and permanent.

It was a public attestation. The mark on the wall was a statement to any neighbor, any passing pedestrian, any potential buyer that this property had been inspected, met the company's standards, and was insured. The market for houses in 1752 Philadelphia included buyers who valued the mark and sellers who could ask a premium for properties that carried it. The verification did work in the price of the asset, not just in the price of the insurance.

It was an access guide for the fire brigade. Philadelphia did not have a public fire department in 1752. It had volunteer companies — the Union Fire Company that Franklin had organized in 1736 was one of them — that responded to fire calls and pumped water from the nearest cistern through leather hoses. When a brigade arrived at a burning house, the Fire Mark told them the Contributionship would compensate the volunteer company for time and equipment. Houses without the mark were sometimes still defended, but the marked house had a financial claim on response. The mark organized the response.

Three functions, one piece of metal. Each function reinforced the others. The surveyor's inspection made the price signal credible. The visible mark made the inspection persistent. The brigade-access function gave the homeowner an immediate operational benefit. The homeowner had a reason to maintain the features the inspection required — because the mark only stayed valid as long as the conditions held.

In 1769, seventeen years in, the Contributionship's directors decided the company would no longer insure wooden buildings, or brick buildings with wooden gables. The reason was actuarial: the claims experience on wooden structures was structurally worse, and the carrier could see it. Six years after that, in 1775, the directors declined to renew the policy on Mrs. Lydia Biddle's house because her property had an unlawful wooden bakehouse adjoining it. The bakehouse violated city ordinance. The Contributionship would not write against a violated ordinance.

The verification was strict. The price signal was tight. The mechanism worked because the people who built it built every component of it to talk to every other component.

What happened to the mechanism

The Contributionship model did not survive the scaling of American insurance.

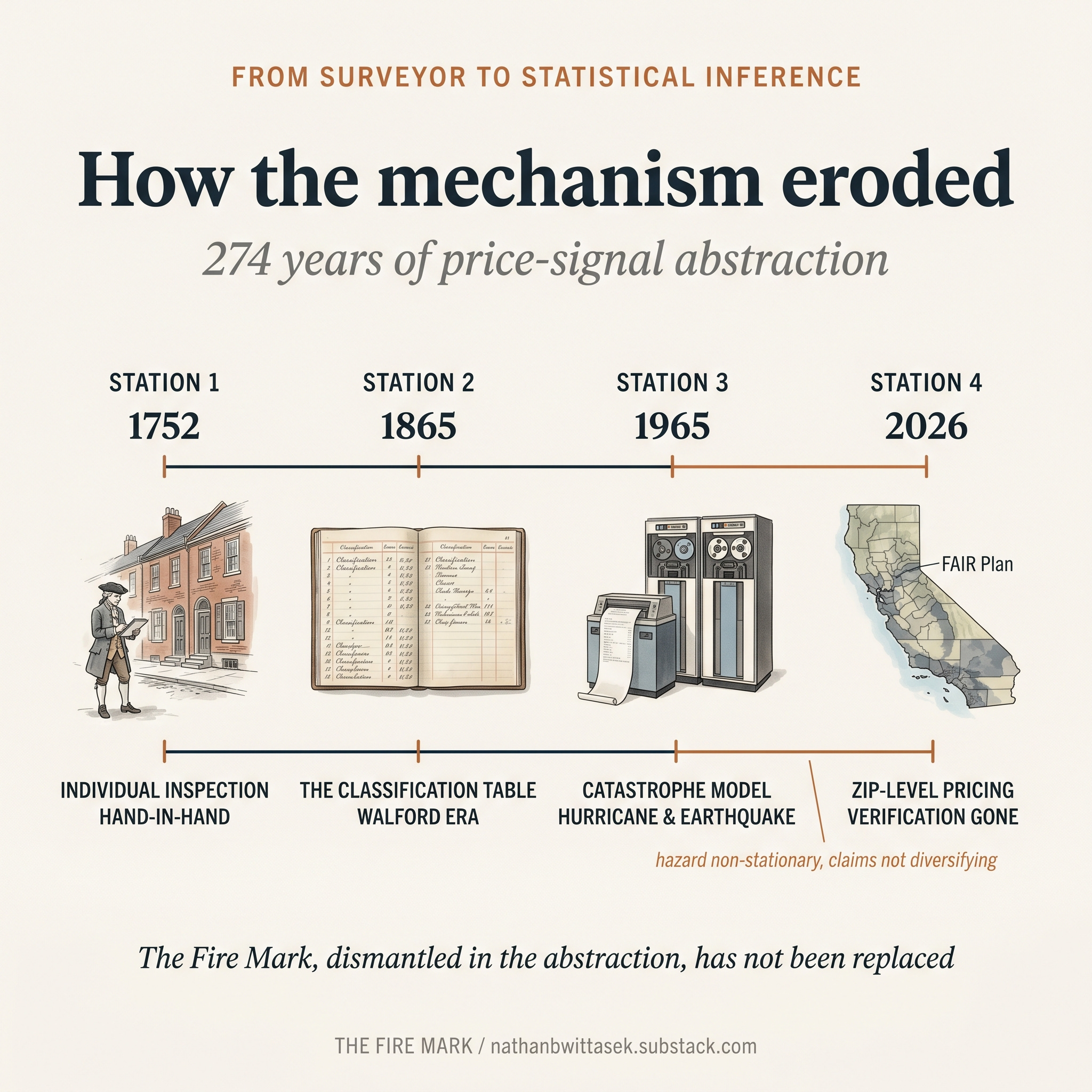

Through the nineteenth century, mutual companies like the Contributionship were joined and then outnumbered by joint-stock fire insurance companies — large carriers writing across geographies far broader than any individual surveyor could inspect. The actuarial revolution that followed, beginning in the 1860s with the work of Cornelius Walford and the U.S. fire-insurance statistical bureaus, replaced the surveyor's individual inspection with the classification table. Exposure was bucketed by construction type, occupancy, neighborhood, fire-district rating. The individual house was priced as a member of its class.

This was the right trade-off for the time. The classification table let a single carrier write thousands of policies a year, across a continental territory, against a labor model that did not require an inspector at every property. Capacity scaled. Granularity dropped.

By the mid-twentieth century, the catastrophe model — beginning with hurricane and earthquake exposure modeling in the 1960s and 1970s — pushed the abstraction further. The carrier no longer priced the individual structure. The carrier priced the ZIP code, the census tract, the watershed, the modeled-event footprint. The Fire Mark was a historical artifact. The verification had been replaced by statistical inference.

This worked for a while. The actuarial machinery was robust enough that the verification gap did not show up as a market failure during the long period when the underlying hazard was stationary and the claims experience was diversifiable across geographies.

The California wildfire crisis is the first time in the modern American insurance market that all three of those conditions have failed simultaneously. The hazard is not stationary — climate, wildland-urban interface expansion, and fuel-load conditions are pushing California claims experience past the historical patterns the actuarial machinery was calibrated to. The catastrophe events are not diversifying across geographies — the January 2025 Los Angeles fires alone triggered a $1 billion FAIR Plan personal-lines assessment, the first in over thirty years. And the underlying parcel-level variation in actual exposure has become large enough that ZIP-level pricing is producing the winner's-curse adverse selection pattern the Boomhower NBER paper documents.

The classification table that worked for a hundred years is no longer doing the work the carrier needs it to do. The price signal is broken. The Fire Mark, dismantled in the abstraction, has not been replaced.

The Two Houses problem in 1752 terms

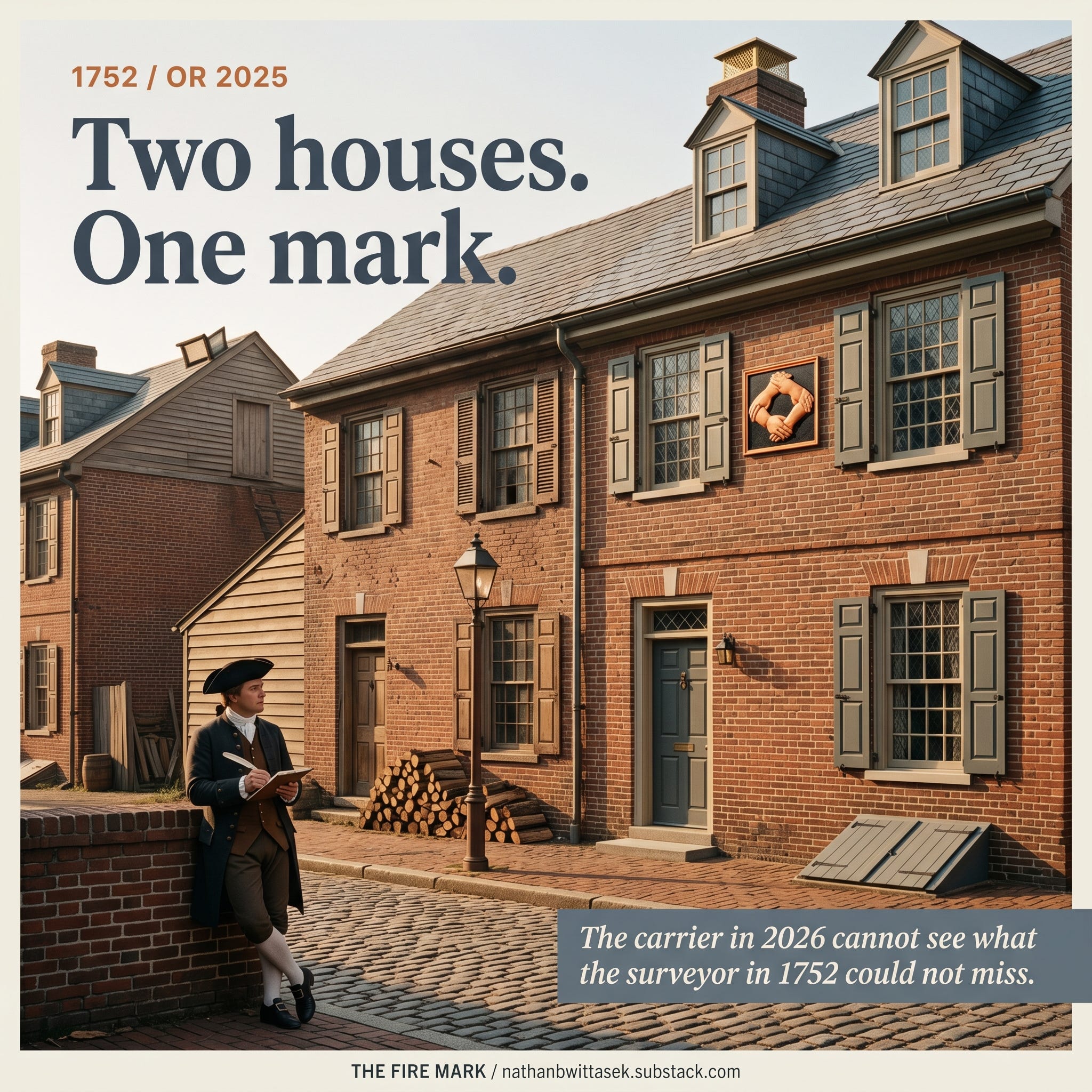

If the Contributionship were writing in Altadena in 2025, the surveyor would have visited both rebuilds.

The surveyor would have looked at the Class A standing-seam metal roof on House B. He would have noted the ember-resistant vent grilles in the boxed-in soffits, the tempered glass on the lee elevation, the five-foot zone of inorganic ground cover between the foundation and the nearest planting. He would have written a memo for the board recommending the policy at standard rate.

He would have walked across the side yard to House A. He would have seen the composite shingle roof, the stucco-finished eaves with the visible underside, the standard wood-framed windows, the ornamental shrubs planted within two feet of the foundation. He would have written a second memo recommending the policy at substandard rate, or with a higher premium charge, or — if his board was sufficiently strict — declining the policy until the homeowner upgraded.

The Fire Mark on House B would have read "Hand-in-Hand, inspected and accepted." House A would not have received a mark. The price signal would have reflected the surveyor's distinction. Owner B's incremental investment in the harder package would have been visible to the carrier the moment the mark went on the wall.

Two hundred and seventy-four years later, the same two houses get the same quote from the same carrier writing the same ZIP. The carrier has no surveyor. The Contributionship's verification mechanism is not part of the system. The IBHS Wildfire Prepared Home certification, which is the closest 2026 equivalent, requires the homeowner to find it, pay for it, document it, and submit it for underwriting review — and even then the discount may or may not land on the policy.

The carrier in 2026 is not refusing to recognize the distinction between House A and House B. The carrier is unable to see the distinction at the granularity the rate filing requires. The verification architecture that was structural to the Contributionship's product is missing from the modern carrier's product.

The owner side of the bargain

This essay has been about the carrier side of the verification architecture. It is half the story.

The Contributionship's policyholder accepted obligations that came with the Fire Mark. Maintain the brick walls. Keep the chimneys swept. Maintain the trap door to the roof so a brigade member could climb up and fight a chimney fire from above. Comply with city ordinances on outbuildings, fuel storage, and combustible materials. Allow the surveyor onto the property at reasonable intervals for re-inspection. If the conditions changed — if the homeowner built an unlawful wooden bakehouse like Mrs. Lydia Biddle — the company could and would decline renewal.

The bargain was symmetric. The carrier inspected and priced. The owner maintained and disclosed. The Fire Mark was the contract made visible.

The 2026 reform path requires the same bargain. The verification architecture has to exist on the carrier side — third-party attestation, parcel-level scoring, rate-filing recognition. It also has to exist on the owner side — and this is where the public conversation has been quieter than it should be. The 2026 California homeowner who wants the partnership the Contributionship offered in 1752 has to be willing to verify the work. To accept inspection as a duty, not a service. To pay for the third-party attestation when the carrier cannot do it directly. To maintain the hardening as a condition of the policy, not just as an option at renewal.

This is the cultural piece that the structural critique often misses. Insurance has historically been a covenant. The covenant has weakened on both sides — the carrier has retreated from inspection, and the owner has come to expect coverage without disclosure. The reform requires both sides to walk back toward the original bargain.

The owner-side responsibility is not a small thing to ask. It is a financial commitment to documentation, inspection scheduling, retrofit maintenance, and occasionally to refusing a carrier that does not honor the work. It is a cultural commitment to seeing the property as a member of a covenant, not a standalone asset. It is a political commitment to defending the verification infrastructure against erosion — voting for state and federal funding for the inspection networks, attesting to the work in public records, supporting block-level participation programs.

This is the part the property owner has to lift. The system around them has to be lifting at the same time. Neither side does it alone.

What the modern Fire Mark looks like

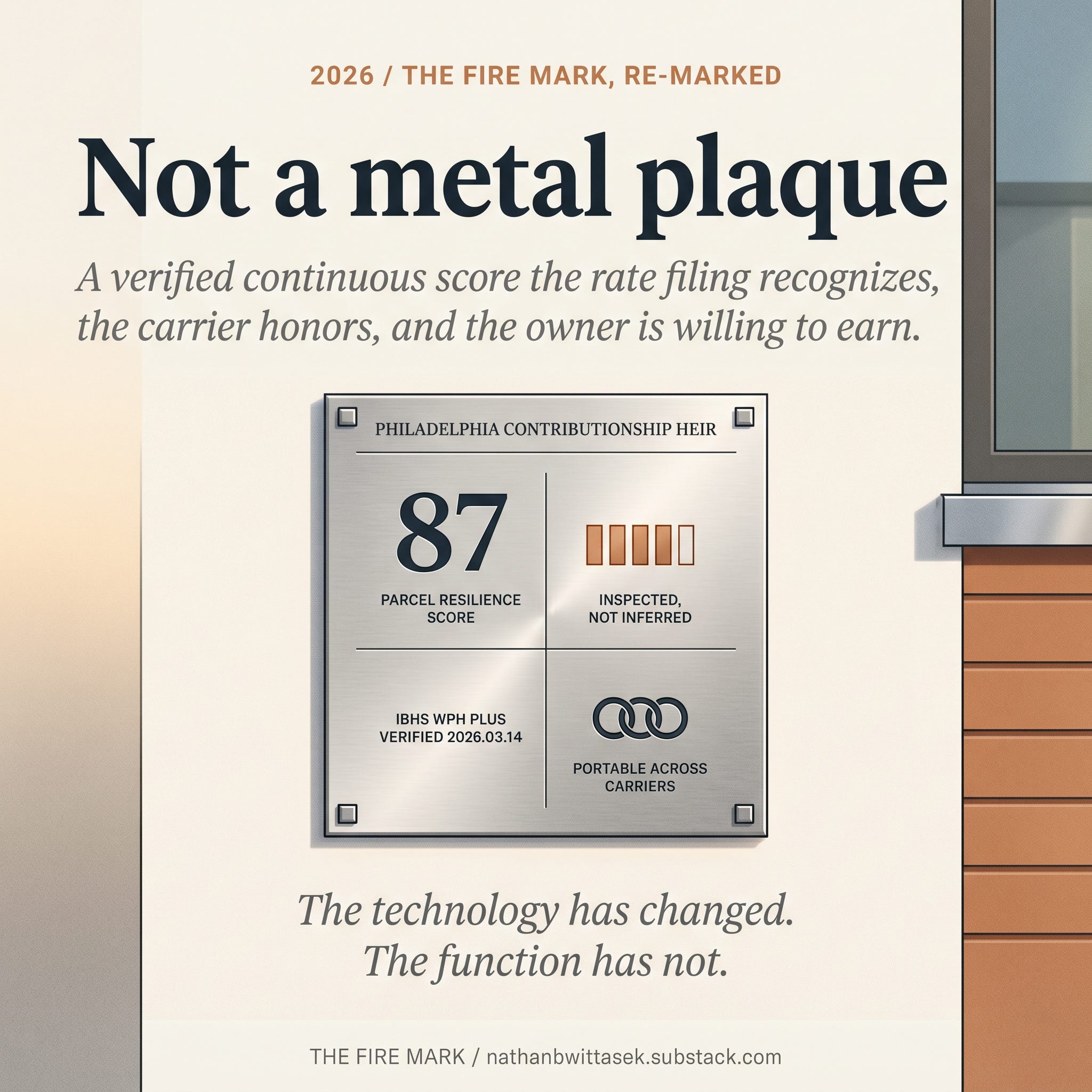

The Fire Mark in 2026 is not a metal plaque.

It is, in technical terms, a continuous parcel-level resilience score, tied to verified inspection data, with an explicit confidence dimension distinguishing inspected from inferred attributes. The score is validated against post-event damage data — the way a credit score is validated against actual default — so the rate filing can defend the score's predictive accuracy in a CDI hearing. The score is portable across carriers, because the value of the verification is destroyed if it is trapped inside one carrier's filing.

The building blocks exist. Cal Fire's post-fire Damage Inspection (DINS) data is published and reflects actual structural performance under fire exposure. The IBHS Wildfire Prepared Home program is an attestation framework with a defined inspection protocol. The California Wildfire Mitigation Program (CWMP) maintains grant records of verified hardening work. Several private parcel-level resilience scoring services have launched in the last three years; one of those services is the platform I run.

None of these is yet a true data commons. None is yet integrated into the standard underwriting and rate-filing workflow at the scale California needs. The integration is the unfinished work.

The Contributionship's surveyors did not have the technology any of these modern services use. They had a notebook, a pen, and walking shoes. The work product was the same: an inspected, attested, visible price-signal-bearing assessment of the property. The technology has changed. The function has not.

The reform path is to rebuild the function with the modern technology. Standard data definitions across the public and private attestation programs. A regulatory framework that recognizes third-party attestation in CDI rate filings with the weight the Contributionship's surveyors carried with their own board. A privacy-and-portability layer that lets the verification follow the parcel across carriers, owners, and refinance events. An explicit, transparent, means-tested affordability mechanism — operated outside the discount table — that handles the equity-and-efficiency tradeoff the granular pricing produces. A property-owner culture that accepts verification as part of the covenant.

This is the unsexy work. It is the work that has been waiting since the last surveyor closed his notebook on the last 1752 Philadelphia row house.

The covenant, re-marked

The two Altadena rebuilds at the start of this essay are eight feet apart, on a block where every house is in some stage of post-fire rebuilding. Six of them have hardened to a meaningful extent. Two have not. Three of the eight have already been quoted the same premium by the same carrier writing the ZIP. The Fire Marks that should be on three of those walls — and not on five — are not on any of them. The carrier cannot see who has done the work.

In Philadelphia, in 1775, the Contributionship's directors looked at Mrs. Lydia Biddle's unlawful wooden bakehouse and declined her renewal. They knew about the bakehouse because the surveyor had walked the property. The surveyor knew to walk the property because the company had been built around the surveyor's visit. The visit was the product.

In California, in 2026, the carrier writes the ZIP because that is what the rate filing currently permits. The carrier does not visit. The carrier does not know. The carrier cannot price the Lydia Biddles or the Owner Bs of Altadena differently than their neighbors because the verification has been removed from the product.

The fix is not nostalgic. It is structural. The Contributionship's mechanism scaled badly past a certain geographic and population threshold; that is why the classification table replaced it. But the technology to rebuild the verification at scale, with statistical machinery the 1752 surveyors did not have, exists in 2026. The standards exist. The data flows exist. The regulatory framework is partway there with the Sustainable Insurance Strategy and the PRID-approved catastrophe models. The owner-side culture is the part that still has to lift.

What the Contributionship got right at the founding is that insurance is a covenant. The carrier sees, prices, and pays. The owner maintains, discloses, and accepts inspection. The mark on the wall is the contract made visible.

That covenant is recoverable. It will not come back as four gilded hands on a black shield. It will come back as a verified continuous score that the rate filing recognizes, the carrier honors, and the owner is willing to earn. That is the Fire Mark, two hundred and seventy-four years on.