The First PRID

Verisk's wildfire model became the first to complete California's PRID review on July 24, 2025 — the most consequential model-review precedent in U.S. property insurance in a generation.

Consumer Watchdog filed its petition to participate in the Verisk PRID with a complaint about notice mechanics. The Department had posted the petition. Consumer Watchdog asked it to be re-posted, and asked the Department to build an email notification system so the public-interest bar could find out about future PRID petitions without combing the CDI website daily. The Model Advisor granted Consumer Watchdog participation. The Model Advisor also ruled — and this is the sentence that decides the future of catastrophe-model intervenor practice in California — that PRID participation does not, by itself, entitle the participant to compensation. Compensation comes only after a later complete rate application relying on the PRID is resolved.

If you are a public-interest lawyer with $200,000 of attorney time on the line for a serious PRID intervention, you have just been told that the check is in the mail when the rate case shows up — which could be eighteen months later, two years later, or never. You either eat the cost up front and hope, or you do not participate.

That single procedural ruling sets the pattern for every future intervenor’s economics in the California PRID system. It came out of the proceeding that produced PRID-2025-00001 — the first Pre-Application Required Information Determination issued by the California Department of Insurance, on July 24, 2025, under California Code of Regulations Title 10, Section 2648.5. The subject was Verisk’s Wildfire Model for the United States V4.0.0, submitted on January 2, 2025 by AIR Worldwide Corporation, doing business as Verisk Extreme Event Solutions, a wholly owned subsidiary of ISO and Verisk Analytics. The determination is valid for four years unless the model is substantively updated, amended, altered, or changed. It does not approve the model for any particular rate filing. It does not relieve any insurer of the burden under Insurance Code Section 1861.05 to demonstrate that a proposed rate is justified. It is a non-adjudicative initial determination of what model information must accompany a future complete rate application that relies on the model.

In other words: PRID-2025-00001 does not change a single rate. It changes what gets disclosed when a rate is changed using this model. And it changes who can afford to be in the room when that disclosure happens.

That is a smaller-sounding outcome than the headlines suggested. It is also a much more consequential one. The PRID process is the first U.S. regulatory mechanism that requires a vendor’s wildfire catastrophe model to be publicly examined as a precondition for pricing use in a major property market. The Verisk PRID is the template that every later California PRID will be measured against. What the Department disclosed and what it kept confidential are both deliberate. Each is load-bearing.

I am a fire engineer. I do not litigate. I read the PRID procedural record the way I read fire-loss investigations, looking for the moment a system was either built to admit the truth or built to keep it out. The two-stage transparency design — confidential technical review first, public disclosure later — is a defensible administrative bargain. It is also a constrained form of public participation. The first carrier to file a rate application using this PRID will discover which it is.

This essay walks the regulatory framework, the Verisk proceeding’s record, what the Department actually said it reviewed, what remains confidential and why, and what the precedent means for the catastrophe-model vendors still in the queue and the state DOIs outside California watching what California has built.

What PRID actually is

California’s Pre-Application Required Information Determination process was established by the Department of Insurance’s catastrophe-modeling regulations, filed and operative December 12, 2024. The regulations codified the framework under 10 CCR § 2644.4.5 (permitting catastrophe models for wildfire exposure in qualifying residential and commercial property insurance), 10 CCR § 2648.5 (establishing the PRID procedure), and 10 CCR § 2644.4.8 (the market-access commitment that conditions catastrophe-model use on insurer commitments to expand writing in wildfire-distressed areas).

The statutory base is Proposition 103, particularly Insurance Code §§ 1861.05, 1861.07, 1861.09, and 1861.10. Section 1861.05 imposes the prior-approval-and-burden-of-proof regime. Section 1861.07 establishes California’s unusually strong public-inspection rule for rate-proceeding information. Section 1861.10 authorizes public participation and intervenor compensation in article 10 proceedings. PRID inherits all of those obligations and adds a procedural overlay specifically designed for catastrophe-model methodology review.

The Department’s stated purpose for PRID is to specify, before a complete rate application is filed, all model information and data that the Commissioner will require as part of that future application. The process is voluntary — a carrier can still file a rate application that uses a catastrophe model without first completing a PRID, but if it does, the full wildfire catastrophe model checklist must accompany the rate filing at submission. A successfully completed PRID gives the carrier a reusable four-year roadmap for what it must file. Carriers and vendors gain procedural certainty. The Department gains a defensible model-review record. Intervenors gain a structured opportunity to participate in methodology review without waiting for a complete rate proceeding.

The process is built around a new Department of Insurance role: the Model Advisor. The Model Advisor oversees each proceeding, may hire outside consultants with relevant expertise, and controls the course of discovery, expert testimony, motions to compel, and procedural rulings. Petitions to initiate or participate must be publicly noticed within three business days, with three business days for responses and ten business days for rulings. Participation petitions are due within five business days of public notice. The proceeding begins five business days after participation rulings issue. The record must close within ninety business days after the confidentiality order absent good cause, and the PRID must issue within fifteen business days after submission.

The market-access bargain in 10 CCR § 2644.4.8 is critical and frequently underdiscussed. A residential carrier that wants to use catastrophe modeling under § 2644.4.5 must either commit to the 85 percent standard — writing in distressed areas a number of policies equal to its statewide market share multiplied by 0.85 and the statewide distressed-area exposure base — or to a 5 percent increment alternative, with separate provisions for low-premium-volume insurers, commercial property insurers, and commitment modifications. A carrier that fails to fulfill the commitment or make reasonable progress must renounce the commitment in a new filing that cannot use catastrophe modeling. The market-access tie is the structural distinction that makes the California framework unlike any other state’s catastrophe-model review regime. PRID is the procedural lever; the commitment is the policy lever.

The Verisk proceeding

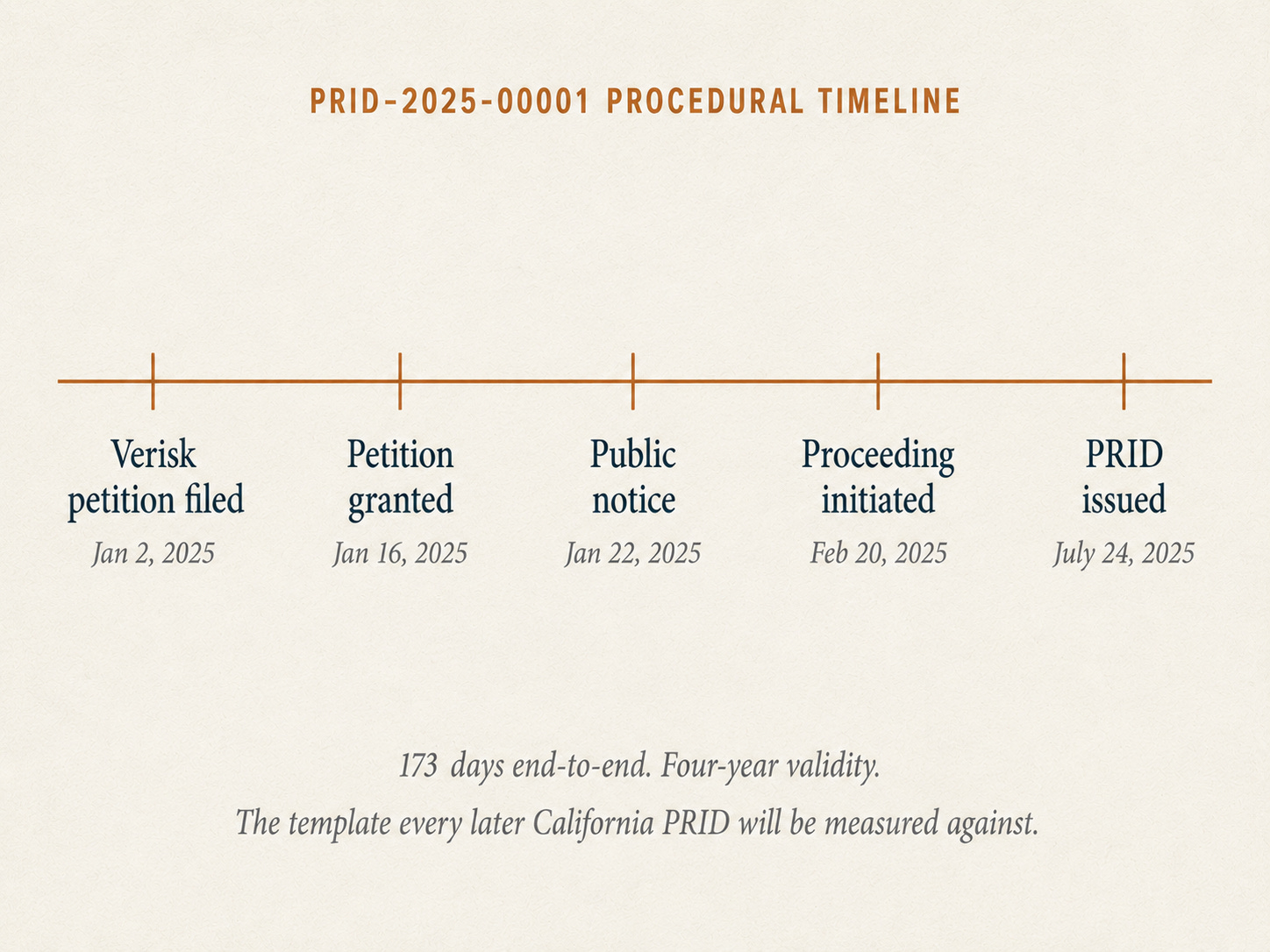

Verisk’s combined petition to initiate and participate in a PRID was submitted on January 2, 2025. The Model Advisor granted the petition on January 16, 2025 and issued the public notice on January 22, 2025. The proceeding was formally initiated on February 20, 2025. The PRID was issued on July 24, 2025. File No. PRID-2025-00001.

The model under review was “Verisk Wildfire Model for the United States V4.0.0.” Verisk’s own public technical materials describe it as event-based and physics-based, designed to capture wildfire risk to property in the 13 westernmost contiguous states. The model uses stochastic weather data and weather-wildfire relationships to generate stochastic wildfire activity, simulates wildfires greater than 100 acres, classifies fire behavior by ecological region, and produces catalogs of 10,000, 50,000, and 100,000 simulated years. The fire-spread component considers fuels, fuel characteristics, terrain, and modeled wind, and explicitly treats surface fire, canopy fire, and ember generation or spotting, with particular attention to wildland-urban-interface spread and suppression. The vulnerability component uses flame length as the intensity variable and incorporates six secondary modifiers, including defensible space and Firewise USA community designation. Verisk’s 2025 wildfire report adds that the model accounts for near-present climate conditions including drought and wind in spread, frequency, and severity, and that the model and the related FireLine tool account for hazard and mitigation actions at or near insured structures.

The public participation set was broader than a conventional actuarial review. The Model Advisor’s January 16 ruling confirms supporting responses from Nationwide, Allstate, and USAA. The participation set ultimately included Stanford’s Climate and Energy Policy Program, Consumer Watchdog, and RAND economist Lloyd Dixon. Consumer Watchdog’s participation petition objected to what it called a lack of meaningful public notice and asked the Department to repost and more clearly publicize PRID petitions, including by creating an email-notification system for interested parties. The Model Advisor granted Consumer Watchdog participation but rejected any reading that PRID itself created a right to intervenor compensation, emphasizing that compensation could be sought only after a later complete rate application relying on the PRID was resolved. That single procedural ruling sets the pattern for every future intervenor’s economics in the California PRID system.

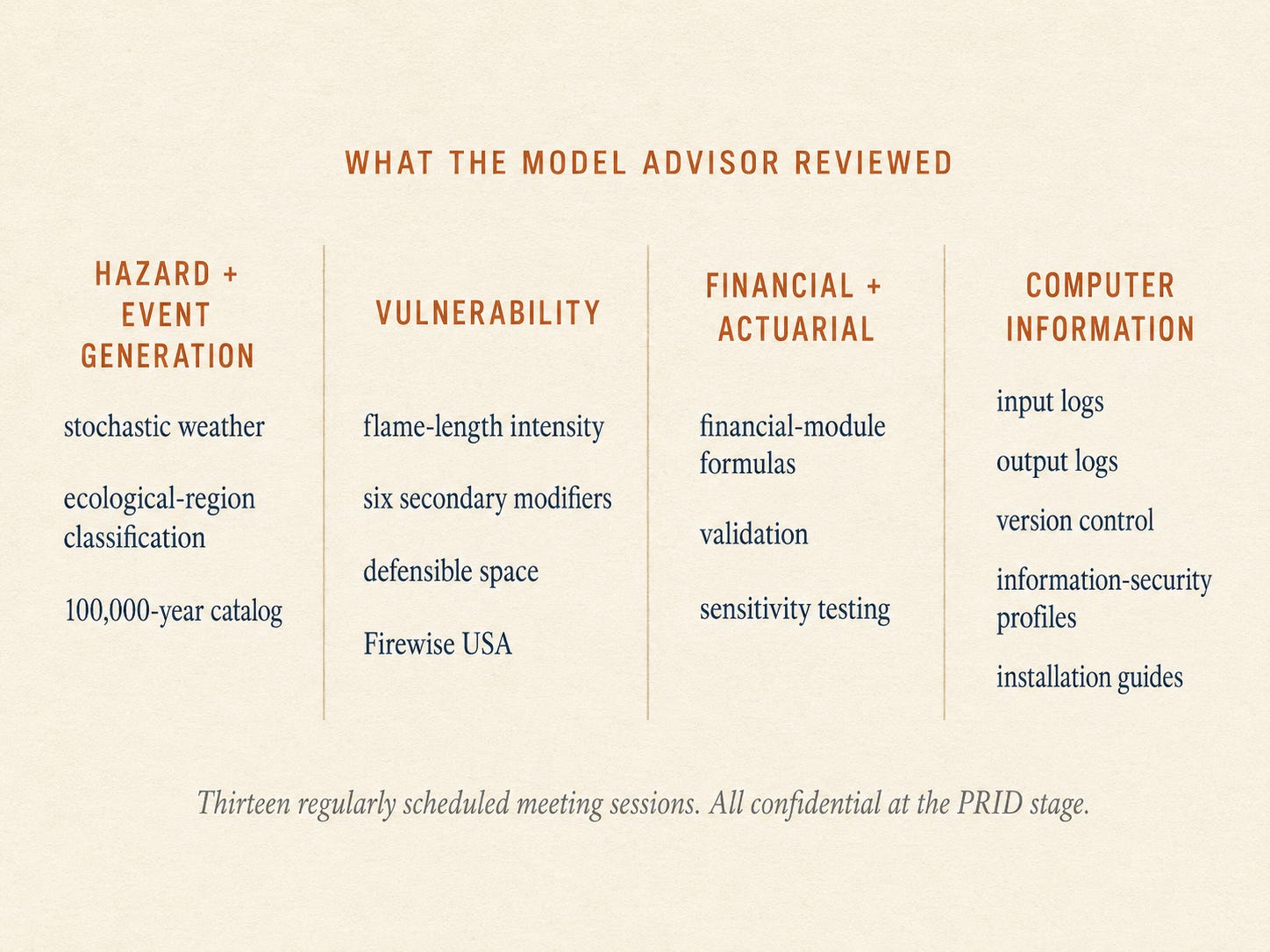

The Department’s July 24, 2025 public notice describes the materials the Model Advisor reviewed. The Advisor examined confidential written documentation from Verisk including model methodology, model input logs, model output logs, a geocoding demonstration worksheet, information-security profiles, installation guides, version-control documentation, and test-case results. The Advisor held thirteen regularly scheduled meeting sessions with the vendor and public participants. The methodology review included an overview, a user-perspective demonstration, and deep dives covering Hazard and Event Generation, Vulnerability, Financial and Actuarial methodology, and Computer Information. The Department used specific instructions and input data to validate and verify the model’s sensitivity to fuels, building and parcel characteristics, and policy terms.

That description is the most informative artifact in the entire public record. The Model Advisor did not perform a perfunctory checklist review. The audit architecture is serious. It is also, by design, confidential at the PRID stage.

What remains confidential, and why

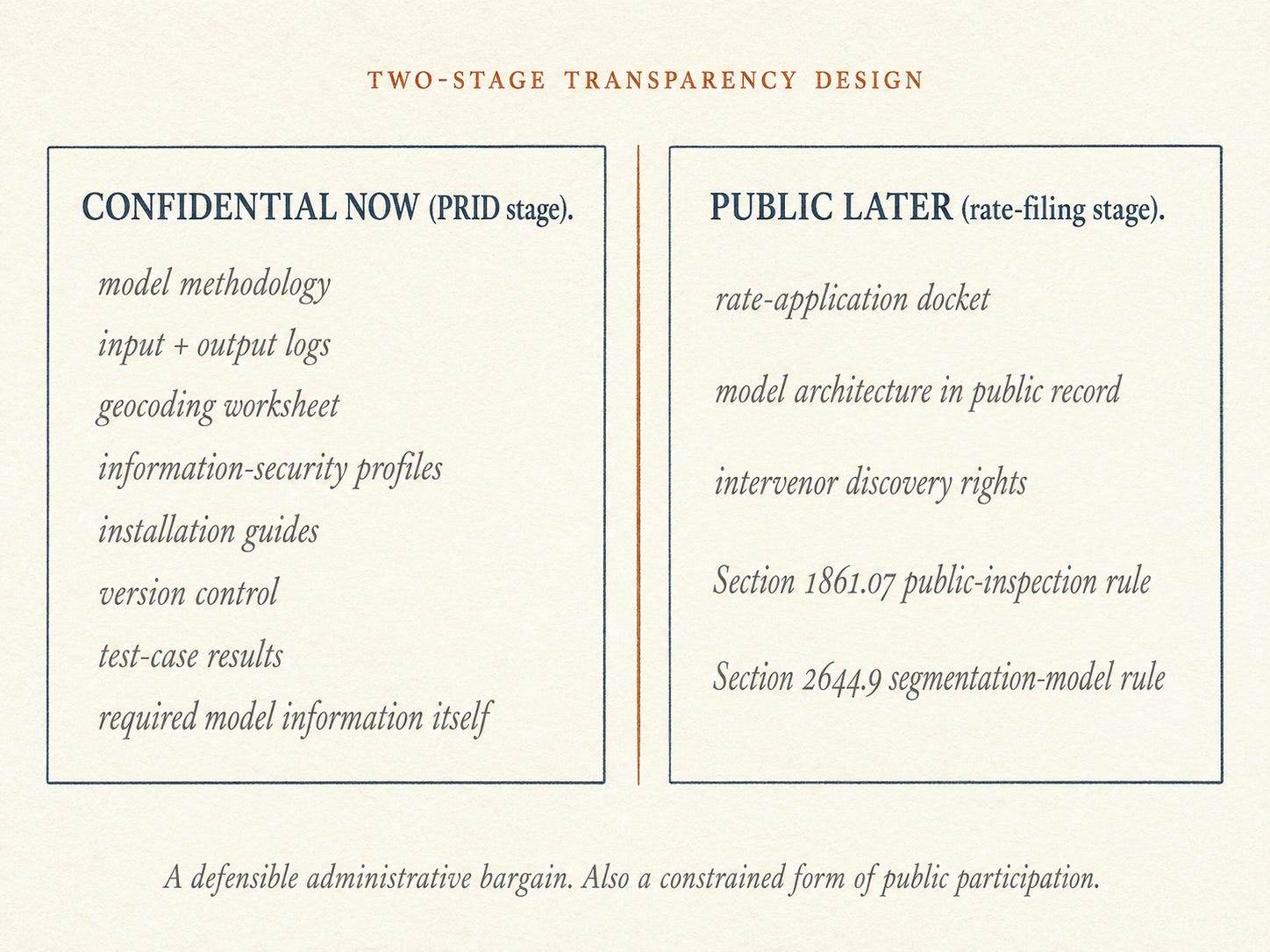

The single most important sentence in the July 24, 2025 public notice is this: the required model information remains confidential until an insurer later submits a complete rate application relying on the model.

That sentence is the core design choice of the California PRID framework. It is also the source of every legitimate transparency critique of the process.

What is publicly available now includes the procedural record (petitions, rulings, public notices, the participation letters, the public webinar, the public checklist), the description of categories of material the Model Advisor reviewed, and the high-level public account of Verisk’s model architecture from Verisk’s own technical documentation and 2025 wildfire report. What is not publicly available includes the exact V4.0.0 hazard equations, California-specific calibration choices, stochastic-event-generation parameters, vulnerability curves, financial-module formulas, geocoding thresholds, sensitivity-test outputs, validation statistics, software controls, and the actual content of the required model information itself.

The intended design is that these materials become public when an insurer first uses the Verisk PRID in a complete rate application. At that point, 10 CCR § 2644.9 (California’s separate, transparency-heavy rule for wildfire risk models used in rating segmentation) and Insurance Code § 1861.07 (the public-inspection command for article 10 proceedings) both apply with full force. The catastrophe model that supported the rate application becomes a public-record matter. Any intervenor in that rate proceeding can then examine, challenge, and depose on the model methodology in a way that the PRID procedure does not allow.

That two-stage transparency structure — confidential technical review first, public disclosure later — is a defensible administrative bargain. It allows the Department to perform a serious technical review without forcing vendors to make their core methodology public before any specific commercial application. It also keeps the deeper merits questions out of PRID, which is by regulation non-adjudicative.

It is also a constrained form of public participation. The intervenors who would most want to test the model’s substantive merits cannot fully do so at the PRID stage. The discovery they can obtain is bounded by what the Model Advisor permits. The compensation framework that makes public-interest participation viable in ordinary Proposition 103 proceedings is, per the Model Advisor’s ruling on Consumer Watchdog, available only after a later complete rate application is resolved. The fight is deferred, not eliminated.

For the first carrier that files a complete California rate application using the Verisk PRID, the deferred fight will arrive. The PRID-required model information will become public. The full rate-filing record will be available for inspection. The merits questions that PRID brackets — does this model produce the most actuarially sound estimate of projected catastrophe losses, does it properly account for the best available scientific information on mitigation at the property, community, and landscape scales, does the carrier’s particular use of the model conform to filed expectations — will all be live. The first such rate filing will be the proceeding that tests whether the PRID framework actually works as designed.

The other models in the queue

The Department’s August 1, 2025 press release on completed model reviews indicated that additional model reviews were in progress under the Sustainable Insurance Strategy. The Verisk PRID was specifically identified as the first. The public record reviewed for this essay does not enumerate every model currently in the queue with the procedural specificity available for the Verisk proceeding, and any reader engaged in current California rate-filing practice will have access to docket information beyond what is publicly summarized here. What is clear is that the procedural template established by PRID-2025-00001 will be the procedural template against which every subsequent California catastrophe-model review is benchmarked.

Several observations follow from that. First, vendor preparation cost is now non-trivial. The Verisk record shows that thirteen meeting sessions, multi-track methodology deep dives, geocoding demonstrations, input-and-output log review, version-control documentation, and test-case results were all part of the Model Advisor’s review. Vendors planning to seek future California PRIDs should expect to assemble a standing regulatory bundle for each model version — version-delta memorandum, California-specific mitigation mapping, validation summary, reproducibility protocol, change-control register, and carrier-facing worksheets designed for later public release in a rate filing.

Second, intervenor preparation is now strategic. Consumer Watchdog’s pattern of early-stage participation, formal objection to notice mechanics, and preservation of compensation theories for later rate proceedings is the playbook other intervenors will follow. The strongest intervenor questions at PRID are usually not “is this rate excessive” but rather “what exactly is the version, what changed from prior versions, how are mitigation variables represented, what can be reproduced from logs and test cases, what anti-duplication plan exists among public participants, is the claimed confidentiality genuinely necessary, and what later carrier choices will still remain open.” Counsel preserving those questions early sets up later challenges in the rate case itself.

Third, the precedent will not stay confined to California. State DOIs outside California — the NYDFS, the Colorado DOI, the Florida OIR (which has its own Hurricane Loss Projection Methodology Commission for hurricane models but no comparable wildfire mechanism), the Oregon DCBS, the Texas DOI — are watching the PRID framework as one model for catastrophe-model regulatory examination. The exact California regulatory architecture is unlikely to be transplanted whole. The procedural template — Model Advisor review, two-stage confidentiality, structured intervenor participation, version-pinned validity — is much more transplantable than the substantive rules around the 85 percent standard or the California-specific market-access commitments. The next two to four years will reveal which elements of the California template the other state DOIs adopt and which they discard.

What the precedent means for the property exposure scoring market

PRID-2025-00001 is, technically, a procedural document about a single Verisk model version. Structurally, it is the beginning of a national shift in how property-insurance catastrophe-model regulation works.

For commercial catastrophe-model vendors — Moody’s RMS, KCC, CoreLogic, Cotality, the smaller wildfire-specialist vendors — the precedent says that public model-methodology review by a state DOI is now an established operational reality, not a theoretical one. The procedural cost is documented. The transparency-architecture compromise is defined. The intervenor playbook is visible. The vendors that have built standing regulatory bundles for each model version will move faster through the next California PRID and through whatever review mechanism the next state DOI adopts. The vendors that have not will spend the next eighteen months building one.

For commercial property exposure scoring vendors that are not technically catastrophe modelers but produce risk scores from related methodology — Cape Analytics, ZestyAI, Reax, FireFactor, others — the precedent is more indirect but no less real. The PRID framework was built for catastrophe models, and these vendors are not catastrophe modelers. But the logic that put model methodology in front of a state Model Advisor — that a score materially affecting whether a property can be insured should be reviewable by the regulator who oversees the market using it — does not stop at the boundary of formal catastrophe models. California’s 10 CCR § 2644.9 already imposes transparency obligations on wildfire risk models used in rating segmentation, and a property risk score is a short step from a rating-segmentation input. The vendors that treat methodology documentation as a standing capability will be ready when the question reaches them. The ones that treat opacity as a moat will find it was a liability.

That is the precedent. PRID-2025-00001 reviewed one model, fixed a version-pinned validity window, and built a two-stage transparency bargain that defers the substantive fight to the first rate filing rather than resolving it. None of that is dramatic on its face. All of it is the procedural ground on which the next several years of property-insurance model regulation will be argued — in California first, and then in whatever form the other departments choose to adopt. The first PRID is the one every one after it gets measured against.

Nate Wittasek, P.E., is a partner at SGH and the founder of Upresilience. He is Chair of the NFPA Technical Committee on Fire Protection Features (serving NFPA 101, Life Safety Code, and NFPA 5000, Building Construction and Safety Code) and a committee member on NFPA 1140 (Standard for Wildland Fire Protection). Views expressed are his own and do not represent the position of NFPA, its Standards Council, or its technical committees.